Related insights

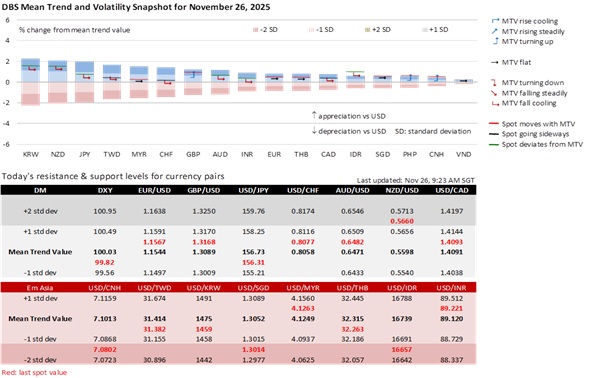

The DXY Index depreciated by 0.4% to 99.8, below the pivotal 100 level for the first time in a week. Markets have revived bets for the Fed to deliver another insurance rate cut at the next FOMC meeting in two weeks, a view reinforced by yesterday’s sharp drop in consumer confidence and a weaker-than-expected ADP report pointing to a softening US labour market. The Treasury 10Y yield eased 2.9 bps to 3.996%, below 4% for the first time in a month, pricing out Fed Chair Jerome Powell’s comment at the October 29 FOMC that a December cut was not a forgone conclusion. A 25-bps cut on December 19 would lower the Fed Funds Rate to 3.75-4.00%. The Fed enters a pre-FOMC blackout period for communications next week.

The US Conference Board reported a 6.8-point tumble in November’s consumer confidence index to a seven-month low of 88.7. Anxiety increased over prices and inflation, tariffs and trade, and politics surrounding the recent government shutdown. Over the next six months, households grew more pessimistic about future business conditions, income prospects, and job availability. Meanwhile, payroll processing firm ADP reported that private companies shed an average of 13.5k jobs per week over the past four weeks, up significantly from 2.5k in the previous update.

Today’s Fed Beige Book will likely reinforce the story of a cooling but not collapsing US labour market, with markets laser-focused on how it describes the labour market, consumer spending, and price pressures. The last report already described employment as largely flat with muted labour demand. Today’s report will likely push a bit further in that direction, with more mentions of hiring freezes and selective outright layoffs. Meanwhile, some surveys also show US consumers planning to cut spending this Black Friday for the first time in years, citing affordability concerns.

GBP/USD’s recovery from 1.30 underscored the soft tone of the USD, especially because GBP has been weighed down for weeks by pessimism surrounding today’s UK Autumn Budget. Markets had largely priced in the UK’s fiscal constraints from Chancellor Rachel Reeves’ self-imposed rules and risk of growth-dampening measures such as tax hikes. GBP/USD may extend its recovery above 1.32 if Reeves delivers the predictability markets seek: a budget that reinforces fiscal prudence, avoids unfunded commitments, and combines growth-friendly measures that align with the Bank of England’s mild easing bias.

Apart from the GBP, the other notable weak currencies to watch for a recovery are the NZD, for the Reserve Bank of New Zealand’s signal that it is at the end of its rate-cutting cycle, and the JPY for intervention risks. After today, expect market activities to slow and positions to be lighter into the long Thanksgiving weekend, encouraging investors to lock in profits. US markets return on December 1, the day the Fed ends quantitative tightening (QT), removing the liquidity scarcity premium that underpinned the USD over the past few years.

Quote of the Day

“Sir, my concern is not whether God is on our side; my greatest concern is to be on God's side, for God is always right.”

Abraham Lincoln

November 26 in history

In 1863, President Abraham Lincoln proclaimed a national Thanksgiving Day to be celebrated every year on the final Thursday of November.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates & Digital Assets)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related insights

Related insights

- Member of Central Deposit Insurance Corporation (CDIC)