Related insights

- Research Library23 Apr 2025

- Singapore’s economy and markets around elections23 Apr 2025

- BlackRock22 Apr 2025

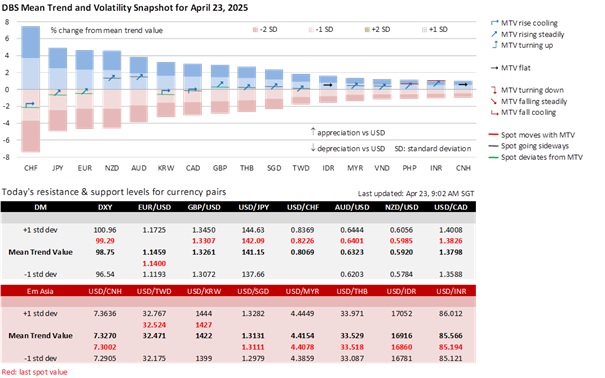

The DXY Index rebounded by 1% to 99.3 after falling below the 100 mark for four consecutive days. The S&P 500 Index rallied 2.5% to 5288 overnight, reversing the 2.4% decline on Monday. The US Treasury 10Y yield eased slightly by one bps to 4.40%.

Market focus shifted from US President Donald Trump’s criticism of Fed Chair Jerome Powell toward renewed hopes of de-escalating US-China trade tensions. US Treasury Secretary Scott Bessent described the ongoing tariff standoff – likening it to a trade embargo – as unsustainable. He emphasized that the US was not seeking to decouple from China and expressed optimism that tensions could ease in the coming months. Trump also raised expectations for reducing the current 145% tariff rate on Chinese imports, contingent on progress toward a trade agreement. Trump added later that he had no intention of firing Powell. Bessent also sought to counter market concerns about a lack of direction in Trump’s agenda by sequencing key initiatives – tariffs were announced on Liberation Day, with a plan to finalize the extension of Trump’s 2017 tax cuts by Independence Day, followed by deregulation efforts.

Despite the IMF issuing the steepest downgrade for US growth among the advanced economies for 2025, the US is still expected to remain the fastest-growing developed nation. Although the IMF lowered US growth to 1.8%, down from 2.7% in January, it remains slightly above the Fed’s March projection of 1.7% and higher than Canada (1.4%), the UK (1.1%), Euro Area (0.8%), and Japan (0.6%). The IMF downgraded this year’s global growth to 2.8% from 3.3%, citing rising worries over the economic fallout from escalating tariffs and trade tensions. Here, markets are paying close attention to the high-level trade talks between the US, Japan, and South Korea. While all sides are eager to demonstrate progress toward a deal, it remains too early to determine whether substantive progress can be achieved to reduce tariffs before the 90-day pause on reciprocal tariffs expires in early July.

Hence, one cannot be too confident that the Trump administration’s more measured tone reflects genuine recalibration. Instead, they were more likely calibrated for the G20 finance ministers and central bank governors’ meetings in Washington on April 23-24. Given Trump’s fixation on maintaining leverage and “holding all the cards” in negotiations, there is little to suggest a lasting shift from his unpredictable and often erratic policy approach. Against this backdrop, G20 nations face mounting challenges navigating the coming global economic and trade activity slowdown. While this week’s meetings offer a platform for dialogue, the path to meaningful cooperation will likely prove elusive. Given the competing forces at play, the recent USD sell-off may transition into a more consolidative phase rather than a sustained reversal. The tug-of-war between Trump’s unpredictable policymaking and the reality of slowing growth amid fragile risk appetite may limit clear directional conviction in the near term.

Quote of the Day

“False hopes are more dangerous than fears.”

J.R.R. Tolkien

April 23 in history

The first YouTube was posted in 2005.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related insights

- Research Library23 Apr 2025

- Singapore’s economy and markets around elections23 Apr 2025

- BlackRock22 Apr 2025

Related insights

- Research Library23 Apr 2025

- Singapore’s economy and markets around elections23 Apr 2025

- BlackRock22 Apr 2025

- Member of Central Deposit Insurance Corporation (CDIC)