Related insights

- Taiwan: Semiconductor tariffs come into effect15 Jan 2026

- JPY Rates: Running with the Takaichi trade15 Jan 2026

- Singapore Equity Picks15 Jan 2026

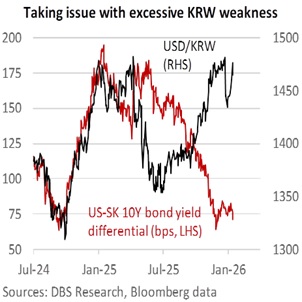

The focus at today’s Bank of Korea meeting is not interest rates but KRW weakness. Persistent concerns over the KRW and its inflationary pass-through have materially constrained the BOK’s room to ease, reinforcing expectations that the policy rate will remain unchanged for an extended period.

The BOK kept the base rate on hold at 2.50% today, following its November upgrade to the growth outlook—1.0% for 2025 (from 0.9%) and 1.8% for 2026 (from 1.6%)—on resilient exports and a gradual recovery in domestic demand. More importantly, inflation risks have firmed. The BOK’s CPI forecasts were raised to 2.1% for both 2025 and 2026, reflecting KRW depreciation and improving demand conditions. Headline inflation has already rebounded to 2.3% YoY in December, from a trough of 1.7% in August, and is now running above the 2% medium-term target. A BOK statement in mid-December warned that inflation could rise to the mid-2% range in 2026 if the KRW remained weak.

Unsurprisingly, the BOK is increasingly alarmed by the KRW’s depreciation bias. On December 24, the BOK and the Finance Ministry issued a statement stating that excessive FX weakness was undesirable and signalled the government’s “strong determination” to stabilize the currency. While this statement briefly drove USD/KRW lower from 1481 to 1434, the move proved short-lived, with the currency pair rebounding to 1476 by January 13. This occurred despite BOK Governor Rhee Chang-yong’s New Year warning that USD/KRW levels in the high 1400s were disconnected from South Korea's economic fundamentals, including strong semiconductor exports.

Recently, USD/KRW retested its November-December highs near 1480, and an overnight pullback to 1465 was triggered by US Treasury Secretary Scott Bessent’s criticism of the KRW’s excessive weakness. While Bessent’s comments did not explicitly endorse FX interventions, his tone reduced the risk that any stabilisation actions by Seoul, which aligns with Washington’s preference for orderly markets rather than one-way depreciation, would be viewed unfavourably.

Overall, the recent price action underscores that verbal intervention alone is insufficient to sustainably turn the KRW. While coordinated statements and external policy signals can slow depreciation and trigger short-term pullbacks, they have failed so far to alter positioning. Absent credible follow-through actual FX smoothing operations, KRW weakness will likely persist above the South Korean policymakers’ comfort zone. Renewed global USD weakness may also be insufficient, given the tight correlation between USD/KRW and USD/JPY and their shared experience with market demand for action rather than rhetoric to reverse weakness in both currencies before they become entrenched.

Quote of the Day

“Mathematics is written for mathematicians.”

Nicolaus Copernicus

January 15 in history

The rules of basketball were first published in Triangle magazine in 1892.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates & Digital Assets)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related insights

- Taiwan: Semiconductor tariffs come into effect15 Jan 2026

- JPY Rates: Running with the Takaichi trade15 Jan 2026

- Singapore Equity Picks15 Jan 2026

Related insights

- Taiwan: Semiconductor tariffs come into effect15 Jan 2026

- JPY Rates: Running with the Takaichi trade15 Jan 2026

- Singapore Equity Picks15 Jan 2026

- Member of Central Deposit Insurance Corporation (CDIC)