Related insights

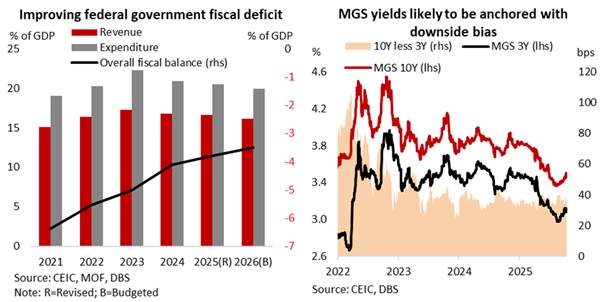

Malaysia’s Budget 2026, announced by Prime Minister and Finance Minister Anwar Ibrahim, reaffirmed the government's continued commitment to fiscal sustainability, even amid more challenging global economic conditions stemming from US tariffs. The administration aims to reduce the federal government budget deficit, as a % of GDP, to 3.5% (MYR74.6bn) in 2026, and to an average of 3.2% for 2026-28 under its medium-term fiscal framework. This marks an improvement from the shortfall of 3.8% (MYR76.7bn) in 2025.

The gradual narrowing of the deficit in 2026 would result from higher planned revenue growth of 2.7% to MYR343.1bn over contained expenditure increase of 1.7% to MYR419.2bn (2.9% and 1.6% growth, respectively, in 2025). Both sides of the ledger would benefit from ongoing fiscal reforms extending into 2026. Government coffers are set to be supported by an expanded sales and services tax (already effective from July 2025), increased efficiency in tax collection through e-invoicing, and other measures like higher duties on cigarettes and alcohol and carbon taxes. These come at a time when real GDP growth is cushioned by domestic resilience despite external headwinds (2026: 4.0-4.5%, 2025: 4.0-4.8%). Spending is projected to be contained by a 14.1% reduction in subsidies and social assistance outlays, despite higher development expenditure increase of 3.1% aimed at sustaining economic competitiveness. Despite several subsidy rationalisation policies including September 2025’s RON95 reform, Malaysia’s inflation remains manageable. This has been due to a calibrated approach that balanced subsidy cuts with the impact on cost-of-living, amid benign global cost conditions. We therefore lower our average headline inflation forecast to 1.4% for 2025 and 2.0% for 2026. Malaysian government securities (MGS) yields have risen from their bottom in mid-August 2025, but muted inflation and prospects for lower net government borrowings due to a smaller fiscal deficit should anchor MGS yields with a downward bias.

Topic

Explore more

E & S Macro StrategyGENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates & Digital Assets)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related insights

Related insights

- Member of Central Deposit Insurance Corporation (CDIC)