Related insights

- FX Tactical Ideas: Momentum to Drive USD Higher26 Jun 2026

- Research Library26 Jun 2026

- Currencies to stabilise after post-FOMC USD frenzy 26 Jun 2026

USTs have recently rallied due to safe-haven demand stemming from the global equity sell-off this week. Easing concern over the Fed’s independence under the New Fed Chair, Kevin Warsh, also drives stronger demand for US govvies and compresses the term premium. The 2Y and 10Y yields have fallen to 4.13% and 4.27% respectively, with the DXY hitting 101.5. However, further downside for UST yields appears limited, in our view. First, the UST auction results have not been constructive, especially against the backdrop of a still-hawkish Fed. The bid-to-cover ratio for 2Y bond sales has dropped from 3.49x to 2.99x, while that for 5Y bonds remains largely on par with the previous issuance at 2.35x. Likewise, demand for 4-week bills and 7Y bonds stays tepid.

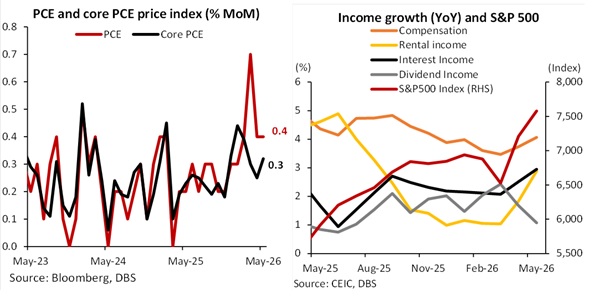

Second, data prints released overnight indicate a firm US economy. Annualised first-quarter GDP is revised upward from 1.6% QoQ to 2.1%. May’s headline and core PCE inflation have increased by 0.4% and 0.3% MoM respectively, with services prices serving as the key drivers. Both personal income and spending are up by 0.7%, beating expectations. Compensation growth accelerates amidst a still-resilient labour market. A robust equity market is supporting consumption sentiment through positive wealth effect, and tax refunds are also fueling spending sentiment. Real personal spending thus heads higher after accounting for inflation. Any upswing in job openings and Non-Farm Payroll prints next week could re-engineer higher UST rates.

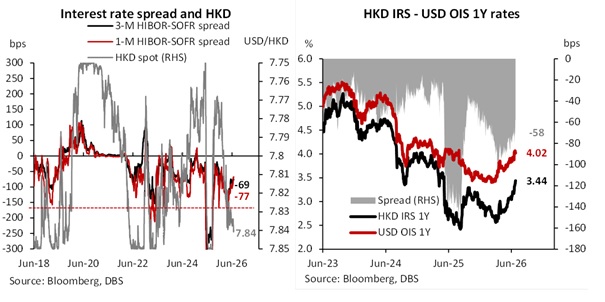

Dollar-pegged HKD rates could see tactical receive opportunities against USD rates. For now, front-end HKD rates are on their upward march. The negative 1Y HKD IRS – USD SOFR spread has already narrowed from -104bps in March to -58bps. Quarter-end settlement effects and the dividend payment season are translating into stronger demand for HKD and higher HIBORs. As seasonal factors fade in mid-July, negative HIBOR-SOFR spreads could once again widen. The weak Southbound flow also adds additional pressure on HIBORs and stresses the HKD.

HKD rates will likely stay volatile as we enter the third quarter. The concurrent narrowing HKD-USD spreads have yet to stall the USD/HKD from heading towards the weak side of the trading band. The strength of the USD and the subsequent pressure on Asian currencies are overriding the impact from higher HKD rates. As the spread is set to narrow on fading seasonal effects, the odds for potential HKMA intervention are stacking up at the margin, albeit remaining conditional on USD strength.

To unsubscribe, please click here.

Topic

Explore more

E & S Macro StrategyGENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates, Digital Assets or Commodities)[1]

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

[1] This disclaimer may not apply if the applicable assets fall within the definition of 'financial instruments' that are set out in Article 2(1) EU MAR (e.g. financial instruments that are traded on a regulated market, MTF or OTF, etc.). Section C of Annex I of MiFID2 specifies these 'financial instruments'.

Related insights

- FX Tactical Ideas: Momentum to Drive USD Higher26 Jun 2026

- Research Library26 Jun 2026

- Currencies to stabilise after post-FOMC USD frenzy 26 Jun 2026

Related insights

- FX Tactical Ideas: Momentum to Drive USD Higher26 Jun 2026

- Research Library26 Jun 2026

- Currencies to stabilise after post-FOMC USD frenzy 26 Jun 2026

- Member of Central Deposit Insurance Corporation (CDIC)