Related insights

- Asia ex-Japan Equities06 Apr 2026

- Conocophillips06 Apr 2026

- USD Rates: No policy dilemma06 Apr 2026

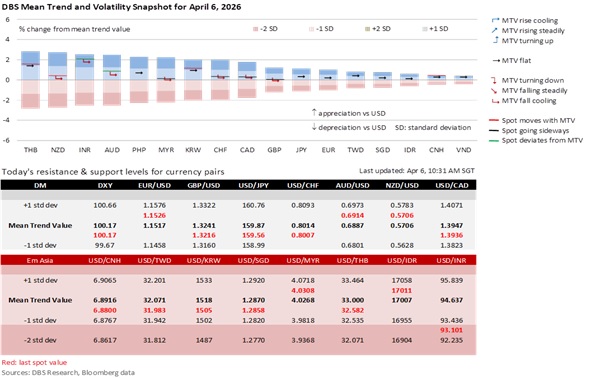

The USD Index (DXY) has been confined mostly to a 99.0-100.5 range since March 11, serving as a dual-axis barometer for the White House’s intentions regarding the Iran War and subsequent monetary policy implications.

On one side, the DXY reflects the uncertainty surrounding President Donald Trump’s Operation Epic Fury. The market is caught between the President’s victory-lap rhetoric (suggesting strategic objectives are nearing completion) and the lack of a clear and credible diplomatic off-ramp. This keeps a war premium floor under the DXY while capping gains on hopes of a near-term de-escalation.

On the other side, the DXY captures a Fed in transition. While the +178k March NFP print exceeded expectations and cast doubt on the sole projected rate cut from the March Summary of Economic Projections (SEP), it has not been enough to trigger a DXY breakout. The Fed’s persistent wait-and-see narrative has successfully held the market back from pricing in actual rate hikes. Reflecting this, the US Treasury 10Y yield peaked at 4.48% on March 27 and eased to 4.34% last Friday, with 4.30% remaining as a pivotal support level.

Meanwhile, President Trump has extended the ultimatum to Iran a third time from April 6 to April 7 (8pm Eastern Time), referring to it as “Power Plant Day and Bridge Day” if Iran continues to keep the Strait of Hormuz closed. The extension follows a weekend of high tension that included the rescue of a downed American crew member from a downed fighter jet and reports of indirect negotiations involving Egypt, Turkey, and Pakistan with Tehran.

President Trump’s extensions appear to be a stalling tactic to force an Iranian capitulation before his 60-day window for unauthorized military action under the War Powers Resolution of 1973 approaches its April 28 deadline. Trump is likely aware of a constitutional showdown he might not win over a war that has eroded his domestic and international standing. First, more "America First" Republicans and independents are turning against the war, fearing it has evolved from a surgical strike into another "forever war." Second, approval of Trump’s economic handling has hit a career low, with voters seeing their purchasing power decimated by a "war-tax" at the pump and in grocery stores. Third, Trump has alienated traditional allies in Europe and the Gulf who are prioritizing economic survival over participating in an illegal war involving potential war crimes under international law.

USD/JPY appears overextended as it tests Japan’s policymakers’ 160 pain threshold. The market is caught between the positive US-Japan interest rate differential supporting USD/JPY and increased expectations (67% chance) for a Bank of Japan rate hike at its April 28 meeting. In Tokyo, the policy consensus is getting clearer that protracted JPY weakness, once viewed as a boon for exporters and the Nikkei 225, is now a primary cost-push inflation threat eroding household purchasing power. The BOJ’s Tankan Survey also reinforced this hawkish shift, highlighting inflation expectations while indicating sufficient corporate sentiment to absorb a 25-bps hike without tipping the economy into recession.

Quote of the Day

“You cannot create experience. You must undergo it.”

Albert Camus

April 6 in history

US’s entry into World War I in 1917 created “Liberty Bonds,” which changed the structure of the US National Debt and retail investing.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates & Digital Assets)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related insights

- Asia ex-Japan Equities06 Apr 2026

- Conocophillips06 Apr 2026

- USD Rates: No policy dilemma06 Apr 2026

Related insights

- Asia ex-Japan Equities06 Apr 2026

- Conocophillips06 Apr 2026

- USD Rates: No policy dilemma06 Apr 2026

- Member of Central Deposit Insurance Corporation (CDIC)