Related insights

- Asia ex-Japan Equities09 Mar 2026

- Research Library09 Mar 2026

- The USD’s fractured haven appeal09 Mar 2026

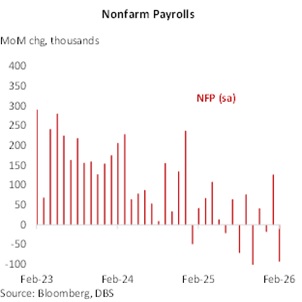

The miss in NFP adds the specter of stagflation into the mix. NFP printed -92k, against consensus of 55k. Judging from the volatility of NFP over the past few quarters, there is a high degree of randomness. This round’s weakness was blamed in part to strikes and bad weather and came about after other high frequency labour market stayed firm (ADP employment and jobless claims). For what it’s worth, the last three months of NFP averaged 5.7k, an improvement from -7.6 in the preceding three months. There is also no turnaround in the shedding of manufacturing jobs thus far. Between the weak NFP print and a mild uptick in the unemployment rate, some caution on the labour market is warranted.

USD rates are conflicted and trading nuanced. US yields across the curve have pushed higher amidst the rapid climb in energy prices. Even if the Iranian conflict ends, it does not guarantee a rapid normalization of energy flows (both production and transport) out of the region. Brent Crude has pushed above USD 90/bbl with WTI just close behind. Inflation expectations are being nudged higher with 2Y breakevens up by close to 90bps since the start of the year. That said, trading in the front of the curve is nuanced and is reflected by the whipsaw on Friday. Yields were pushing higher before the unexpectedly weak NFP hit. However, inflation worries still took 2Y yields higher before they eventually settled below 3.60%. We think real frontend rates would probably be compressed as policy making becomes conflicted.

The back of the curve is similarly conflicted. The back end of the curve has to consider haven demand (bringing yields lower), economic conditions (some weakness due to NFP), higher inflation (due to energy prices) and spillovers from other G10 yields (higher due to energy prices). Yields will probably be stuck in range until a more dominant narrative takes shape. Interestingly, the curve steepened modestly even as the spectre of stagflation looms. This can probably be attributed to significant haven demand already pre-positioned over the past few weeks as the 2Y/10Y segment flattened from a peak of 73bps in early Feb to 58bps currently.

Topic

Explore more

E & S Macro StrategyGENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates & Digital Assets)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related insights

- Asia ex-Japan Equities09 Mar 2026

- Research Library09 Mar 2026

- The USD’s fractured haven appeal09 Mar 2026

Related insights

- Asia ex-Japan Equities09 Mar 2026

- Research Library09 Mar 2026

- The USD’s fractured haven appeal09 Mar 2026

- Member of Central Deposit Insurance Corporation (CDIC)