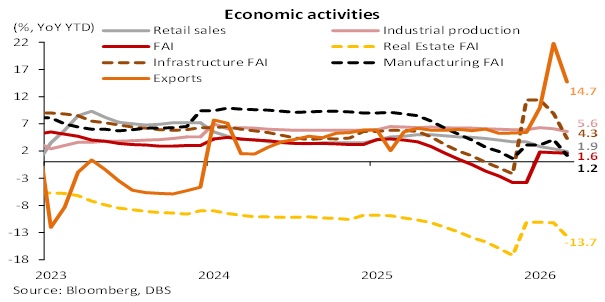

- Trade momentum remained robust, supported by the AI-related electronics upcycle.

- Industrial activity softened amid war-related uncertainty and ongoing “anti-involution” measures.

- Retail sales slow amid weaker income, rising unemployment, and higher savings preference.

- Investment and credit growth all stayed subdued.

- Diversified imports sources and strong renewable penetration reduce vulnerability to oil shocks.

Related insights

- Fixed Income Weekly: Peace Hopes Drive Rates Relief28 May 2026

- Research Library28 May 2026

- Rates: Deal optimism, hawkish shifts & policy divergence 28 May 2026

Click here to read the full report

China’s economy continued to show a clear dual-speed pattern, with external demand remaining resilient while domestic demand stayed relatively weak. Export growth was solid and supported by the ongoing AI-related electronics upcycle as well as sustained competitiveness in global trade. Industrial activity moderated amid heightened geopolitical uncertainty and the continuation of “anti-involution” measures aimed at reducing excess capacity and disorderly competition in key sectors. On the domestic side, retail sales slowed as income growth decelerated and unemployment pressures increased. Households also maintained a higher precautionary savings preference which weighed on consumption momentum. Investment and credit growth remained subdued due to cautious business sentiment, lingering property sector weakness, and limited appetite for expansion. At the same time, China’s macro resilience was supported by structural shifts. These include more diversified energy import sources and rapid renewable energy penetration which reduced exposure to oil price shocks. Separately, RMB internationalisation continued to progress. Usage of CNY in trade finance increased and adoption of the Cross-border Interbank Payment System (CIPS) also rose. This trend was reinforced by heightened geopolitical tensions and efforts to reduce reliance on traditional settlement currencies.

Click here to read the full report

Nathan Chow 周洪禮

Senior Economist and Strategist - China & Hong Kong 高級經濟學家及策略師 - 中國及香港

[email protected]

Subscribe here to receive our economics & macro strategy materials.

To unsubscribe, please click here.

Topic

Explore more

E & S FocusGENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates, Digital Assets or Commodities)[1]

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

[1] This disclaimer may not apply if the applicable assets fall within the definition of 'financial instruments' that are set out in Article 2(1) EU MAR (e.g. financial instruments that are traded on a regulated market, MTF or OTF, etc.). Section C of Annex I of MiFID2 specifies these 'financial instruments'.

Related insights

- Fixed Income Weekly: Peace Hopes Drive Rates Relief28 May 2026

- Research Library28 May 2026

- Rates: Deal optimism, hawkish shifts & policy divergence 28 May 2026

Related insights

- Fixed Income Weekly: Peace Hopes Drive Rates Relief28 May 2026

- Research Library28 May 2026

- Rates: Deal optimism, hawkish shifts & policy divergence 28 May 2026

- Member of Central Deposit Insurance Corporation (CDIC)